It’s surprisingly simple, yet accountants suggest not enough business owners do it – often causing undue stress and difficulties down the track.

Tom’s comment: Individuals could greatly benefit from this too! In fact, why don’t you make this one of the grat ideas you implement to kick off the new year?

http://www.mybusiness.com.au/growth/2572-the-accounting-trick-you-ve-probably-overlooked

Watch Out For People

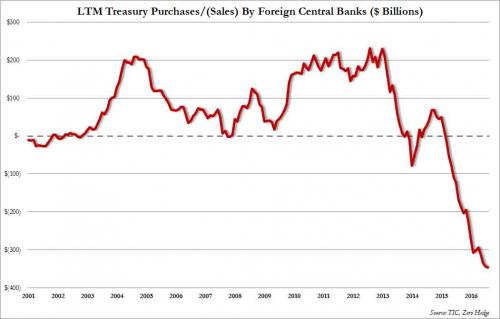

Saudis and China Dump Treasuries; Foreign Central Banks Liquidate A Record $346 Billion In US Paper

One month ago, when we last looked at the Fed’s update of Treasuries held in custody, we noted something troubling: the number dropped sharply, declining by over $27.5 billion in one week, the biggest weekly drop since January 2015, pushing the total amount of custodial paper to $2.83 trillion, the lowest since 2012. One month later, we refresh this chart and find that in the latest weekly update, foreign central banks continued their relentless liquidation of US paper held in the Fed’s custody account, which tumbled by another $22.3 billion in the past week, pushing the total amount of custodial paper to $2.805 trillion, another fresh post-2012 low.

http://www.zerohedge.com/news/2016-10-18/saudis-china-dump-treasuries-foreign-central-banks-liquidate-record-346-billion-us-p

15 Body Language Blunders Successful People Never Make

4 myths about selling a business debunked

If you run a business there is some good information in here.

http://www.mybusiness.com.au/growth/2155-4-myths-about-selling-a-business-debunked

BIG BANK CUSTOMERS TO BE DESTROYED IN NEXT ECONOMIC MELTDOWN: HELEN CHAITMAN

Greg Hunter interviews Helen Chaitman, author of the book ‘JPMadoff’, which describes the complicity of the “Too Big to Fail” bank, JPMorgan-Chase in the $64 billion Bernie Madoff fraud against his clients. She is also the lead attorney in an ongoing lawsuit against JPMorgan-Chase. Her website, JPMadoff.com has links to 1,100 pages of documentation, proving their decades-long pattern of fraud.

Helen describes how JPMorgan-Chase is hardly alone among the “Too Big to Fail” banks and that she could have just as easily have written the book about any of the other ones but the notoriety of the Bernie Madoff case and of his conviction make the story of this bank more accessible to the general public.

Chaitman says that she can’t get arrested to do an interview on a mainstream news show because the government and the media are complicit in these crimes. The latter accept advertising dollars from them and run their commercials.

The only interview she was able to get on FOXNEWS was abruptly cut short when she explained that she was suing JPMorgan-Chase – and the host’s earpiece started to crackle and she promptly called an “emergency commercial” and booted Chaitman out of the studio!

http://forbiddenknowledgetv.net/big-bank-customers-destroyed-in-next-economic-meltdown-helen-chaitman-27750

Forget Gun Control We Need Government Control

Well done Brits!

Update on pension entitlement for all

As a self funded retiree, I’m frustrated with Canberra’s continuous fiddle with Superannuation contributions and rule changes, plus the measure to Rebalance the Pension Assets Test to be implemented on 1 January 2017.

So here’s fair warning to all politicians of any persuasion, this group of aged voters may be about to make the greatest impact on any Federal election in history. Ignoring them may be the start of a changed political environment in this country.

Change the Entitlements

I absolutely agree, if a pension isn’t an entitlement, neither is theirs. They keep telling us that paying us an aged pension isn’t sustainable. Paying politicians all the perks they get is even less sustainable! The politicians themselves, in Canberra, brought it up, that the Age of Entitlements is over:

The author is asking each addressee to forward this email to a minimum of twenty people on their address list; in turn to ask each of those to do likewise. In three days, most people in Australia will have this message. This is one idea that really should be passed around because the rot has to stop somewhere.

Proposals to make politicians shoulder their share of the weight now that the Age of Entitlement is over:

1. Scrap political pensions. Politicians can purchase their own retirement plan, just as most other working Australians are expected to do.

2. Retired politicians (past, present & future) participate in Centrelink. A Politician collects a substantial salary while in office but should receive no salary when they’re out of office. Terminated politicians under 70 can go get a job or apply for Centrelink unemployment benefits like ordinary Australians. Terminated politicians under 70 can negotiate with Centrelink like the rest of the Australian people.

3. Funds already allocated to the Politicians’ retirement fund be returned immediately to Consolidated Revenue. This money is to be used to pay down debt they created which they expect us and our grandchildren to repay for them.

4. Politicians will no longer vote themselves a pay raise. Politicians pay will rise by the lower of, either the CPI or 3%.

5. Politicians lose their privileged health care system and participate in the same health care system as ordinary Australian people. i.e. Politicians either pay for private cover from their own funds or accept ordinary Medicare.

6. Politicians must equally abide by all laws they impose on the Australian people.

7. All contracts with past and present Politicians men/women are void effective 31/12/2015.

The Australian people did not agree to provide perks to Politicians, that burden was thrust upon them.

Politicians devised all these contracts to benefit themselves.

Serving in Parliament is an honour, not a career.

The Founding Fathers envisioned citizen legislators, so our politicians should serve their term(s), then go home and back to work. If each person contacts a minimum of twenty people, then it will only take three or so days for most Australians to receive the message. Don’t you think it’s time?

THIS IS HOW YOU FIX Parliament and help bring fairness back into this country! If you agree with the above, pass it on.

If you wonder why the above individuals are asking for your help look at the figures below.

STATUTORY OFFICES

Date of Effect 1 July 2014

Specified Statutory Office

Base Salary (per annum)

Total Remuneration for office (per annum)

Chief of the Defence Force > $535,100 – $764,420

Commissioner of Taxation > $518,000 – $740,000

Chief Executive Officer, Australian Customs And Border Protection Service > $483,840 – $691,200

Auditor-General for Australia > $469,150 – $670,210

Australian Statistician > $469,150 – $670,210

Salaries of retired Prime Minister and Politicians

Salary as of 1 July

Prime Minister $507,338

Deputy Prime Minister $400,016

Treasurer $365,868

Leader of the Opposition $360,990

House of Reps Speaker $341,477

Leader of the House $341,477

Minister in Cabinet $336,599

Parliamentary secretary $243,912

Other ministers $307,329

Shadow minister $243,912

Source: Remuneration Tribunal.

So if I press all the right buttons, the TOTAL annual wages for the 150 seats in the Parliament are: $17,317,752

The TOTAL ANNUAL SALARIES (for 150 seats) = $41,694,311 – PER YEAR!

And that’s just the Federal Politicians, no one else!

For the ‘lifetime’ payment example (below) I used the scenario that:

1. They are paid ‘lifetime’ salaries the same as their last working year and

2. After retiring, the ’average’ pollie’s life expectancy is an additional 20 years (which is not unreasonable).

It’s worth remembering that this is EXCLUDING all their other perks!

SO, for a 20 years ‘lifetime’ payment (excluding wages paid while a Parliamentarian)

Prime Minister @ $507,338 = A$10,146,760

Deputy Prime Minister @ $400,016 = A$8,000,320

Treasurer @ $365,868 = A$7,317,360

Leader of the Opposition @ $360,990 = A$7,219,800

House of Reps Speaker @ $341,477 = A$6,829,540

Leader of the House @ $341,477 = A$6,829,540

Minister in Cabinet @ $336,599 = A$6,731,980

Parliamentary Secretary @ $243,912 = A$4,782,240

Other ministers** @ $307,329 = A$6,146,580 x 71 = A$436,407,180

Shadow ministers** @ $243,912 = A$4,878,240 x 71 = A$346,355,040

Conclusions:

TOTAL ‘life time’ (20 year) payments, (excluding wages paid while in parliament) = A$833,886,220 – OVER $833 MILLION.

Julia Gillard, Kevin Rudd, John Howard, Paul Keating, Malcolm Fraser, Bob Hawke, et al, add nauseum, are receiving $10 MILLION + EXTRA at taxpayer expense.

Should an elected PM serve 4 years and then decide to retire, each year (of the 4 years) will have cost taxpayers an EXTRA Two and a half million bucks a year! A$2,536,690 to be precise.

A 2 year retirement payment cut-off will SAVE our Oz bottom lineA$792,201,909 *** NEARLY $800 MILLION.

There are 150 seats in House, minus the 8 above = 142 seats, divided equally for example = 71 each for both shadow and elected ministers.

This example excludes all wages paid while a parliamentarian AND all perks on top of that – travel, hotels, secretarial staff, speech writers, restaurants, offices, chauffeured limos, security, etc. etc. 150 seats, 20-year payment of A$833,886,220 less annual salary x 2 years of A$83,388,622. [$41,694,311 x 2]

“Instead of giving a politician the keys to the city, it might be better to change the locks.”

YOU’RE RIGHT, YOU HAVE FOUND WHERE THE CUTS SHOULD BE MADE!

ACTION: Push for a MAX 2 year post retirement payment (give ‘em time to get a real job).

Spread it far and wide folks. People should know.

We Can’t Afford

Do Your Own Homework

This might just very well be the most valid post I’ve taken off Facebook!