The truth can be denied. It can be railed against. It can be discredited. It can be slandered. Its source can be villified. But the one thing about the truth, it cannot be disproven.

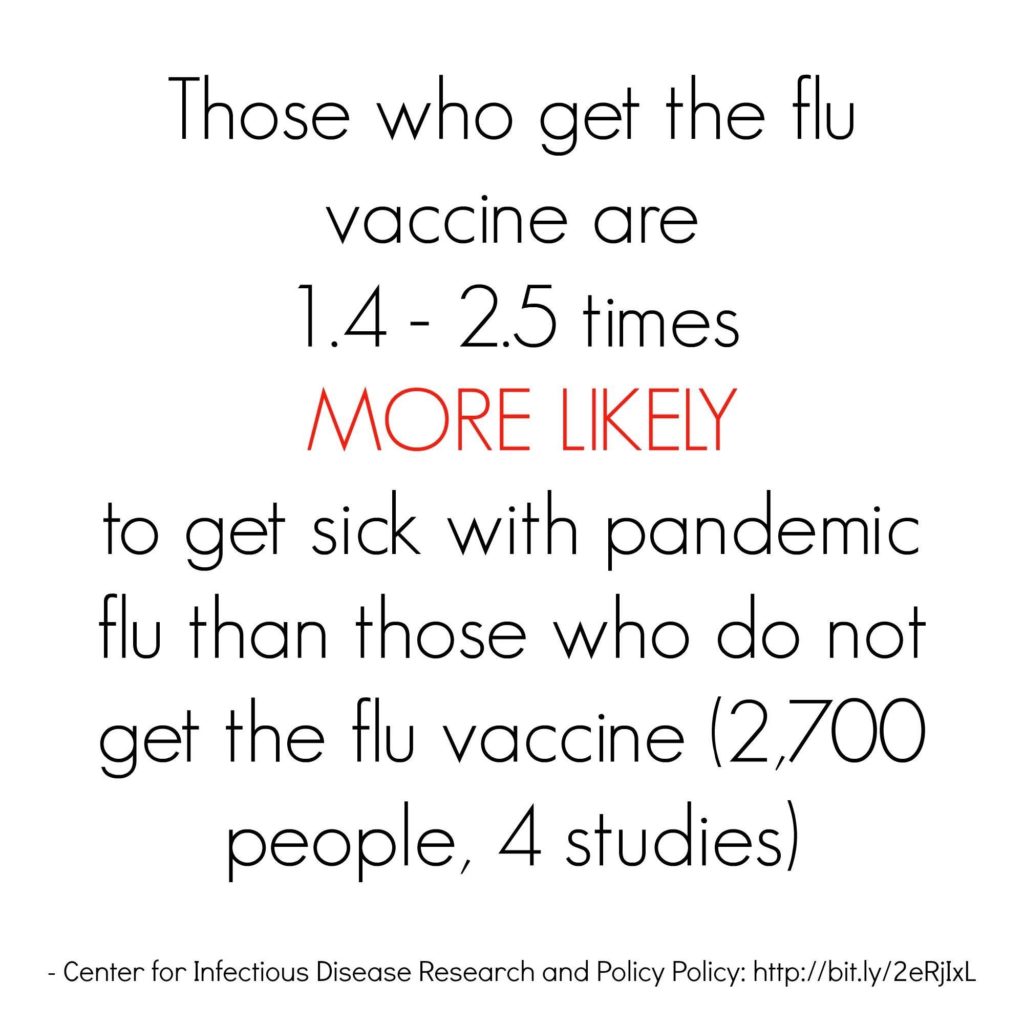

When the US Supreme Court states that vaccines are unavoidably unsafe and the vaccine injury compensation tribunal has paid out 4 billion dollars in damages for vaccine induced death and disablement one cannot say that vaccinnes are safe.

When vaccinated children regularly shed and contract the disease against which they have been vaccinated one cannot honestly claim they are effective.

If they are neither safe nor effective and we have a raging epidemic of childhood chronic disease, when countries with higher vaccination rates have higher infant mortality rates and when unvaccinated kids are proven by survey to be healthier than vaccinated kids we are forced to confront the fact that despite their stated intentions and our hopeful administration of them, they are doing more harm than good.

A report published Wednesday by the French Agency for Food, Environmental and Occupational Health & Safety (ANSES) has warned about “the presence of different hazardous chemicals in disposable diapers that can migrate into the urine and come into prolonged contact with babies’ skin.” The list of chemicals is as long as it is disturbing. In total, ANSES identified some 60 chemicals, including glyphosate, the active chemical in Monsanto’s infamous herbicide Roundup. Some of the pesticides in the report have been banned in the European Union for over fifteen years, such as lindane, quintozene and hexachlorobenzene. Many fragrances, such as benzyl alcohol or butylphenyl were found. PCBs, dioxins, volatile organic compounds (naphthalene, styrene, toluene, dichlorobenzenes, etc.) and polycyclic aromatic hydrocarbons (PAHs), which are usually found in cigarette smoke or diesel engines were also discovered. Since some of these chemicals have demonstrated carcinogenic, mutagenic and reprotoxic (CMR) effects and are considered to be endocrine disruptors, the risks related to their exposure are not limited to the simple skin irritations observed by the vast majority of parents on their babies’ bottoms. https://sustainablepulse.com/2019/01/23/french-safety-agency-discovers-60-toxic-chemicals-including-glyphosate-in-baby-diapers/

Frankincense essential oil, aka the King of Oils, has been proven to speed wound healing, reduce inflammation and stress and promote sleep and fight cancer.

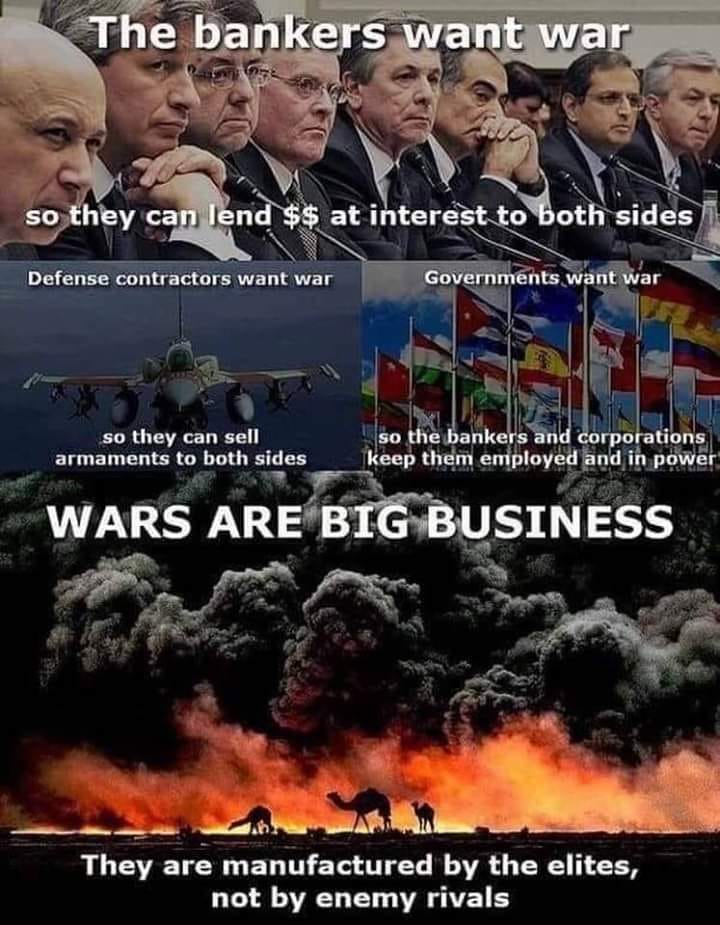

The farce of bail-in is playing out in Australia right now, with the banks complaining to the regulator that they can no longer find suckers to buy the bail-in bonds that are supposed to be their buffer against a crash.

It’s the latest example of why the whole bail-in system should be scrapped, in favour of Glass-Steagall laws that keep deposit-taking banks safe by separating them from risky investment banking and other financial services.

Bail-in is the scheme concocted by the Bank of England following the 2008 banking crash, and implemented through the Bank for International Settlements (BIS) and Financial Stability Board (FSB) based in Basel, Switzerland. Stripped of all of the confusing technicalities, their plan amounts to protecting banks from crashes by increasing their capital buffer against losses, instead of requiring them to stop the reckless financial gambling that causes crises in the first place. The buffer is called Total Loss-Absorbing Capacity (TLAC), at the centre of which are pernicious instruments known as “bail-in bonds”—hybrid securities that are sold as tempting, high-interest bonds, but which, when a bank runs into trouble, convert into effectively worthless shares in the bank.

Bail-in also includes deposits, which the FSB mandates can be written off or converted to shares to save a failing bank. The bail-in systems legislated in the USA, Europe, UK, New Zealand and Canada all include deposits in a bail-in; the Australian government snuck bail-in legislation through Parliament in February 2018, which they denied includes deposits, but which has loopholes big enough to drive a truck through that in an emergency can allow deposits to be bailed in. However, the government doesn’t deny that its legislation includes bail-in bonds.

TLAC

On 8 November 2018, the bank regulator, Australian Prudential Regulation Authority (APRA), issued a paper that said the banks should raise $75 billion in extra TLAC capital by selling more so-called “Tier II” bonds, a.k.a. bail-in bonds.

On 14 January, Jonathan Shapiro reported in the Australian Financial Review that in their responses to the paper the banks asked APRA to reconsider the plan, because it would be too difficult to sell bail-in bonds in the current market.

Shapiro reported: “Westpac treasurer Curt Zuber said he supported the APRA proposal to build a large buffer in the form of Tier II capital in principle but said the global fixed income market had moved away from buying Tier II bonds. ‘As we go through cycles, it is potentially problematic for the banks to get the volumes they need in an economic way for the system which allows for the balance we want to achieve,’ he said.”

This is a major admission, which reflects the growing concern that the financial system is in danger of another crash. With APRA’s encouragement, Australia’s banks were able to sell around $100 billion worth of bail-in bonds over the last 6-7 years. These bonds were very tempting to investors, for two reasons. First, they carried interest rates of up to 8 per cent, offering unbelievably good returns in the post-GFC low-interest environment.

Second, and more importantly, the investors assumed that because the bonds were being issued by Australia’s major banks, which were touted as the strongest in the world, there was no risk that they would be bailed in. That’s assuming they were even aware that these hybrid bonds could be bailed in. While the Bank of England, for instance, forbade British banks from selling bail-in bonds to retail investors, so-called mums and dads, on the basis that they might not understand their full risks, APRA allowed Australia’s banks to aggressively target mum-and-dad investors, to whom they sold bail-in bonds amounting to $43 billion.

The Citizens Electoral Council was the first to warn investors that, contrary to their propaganda, Australia’s banks weren’t safe, and that they were being set up to wear the banks’ losses. In an 8 July 2016 release headlined “Warning to Australian investors: Beware hybrid securities, a.k.a. ‘bail-in’ bonds!”, the CEC warned:

“Australia’s big banks are careening along a cliff’s edge at breakneck speeds with ordinary investors strapped to their bumpers as human shock absorbers. Bank regulator APRA is allowing the big banks to sell to unsuspecting Australian investors products that are illegal for banks in other countries to sell to anyone but other financial institutions.”

On 26 October 2017, Greg Medcraft, the outgoing boss of the Australian Securities and Investments Commission (ASIC), warned in testimony to the Senate that bail-in bonds sold to mum-and-dad investors were “a ticking time bomb”. Medcraft said most investors would not believe that they would be bailed in, but, he emphasised, “Yes, they’ll be bailed in. … Basically, they can be wiped out—there’s no default; just through the stroke of a pen they can be written off. For retail investors … these are very worrying. They are banned in the United Kingdom for sale to retail. I am very concerned that people don’t understand….”

Now, following the revelations of the Hayne Banking Royal Commission and with property prices plunging, the banks are effectively admitting that the market has less confidence in them—there aren’t as many suckers willing to be human shock absorbers. Investors are more aware that if they buy bail-in bonds, there is a very real danger they will be bailed in.

Glass-Steagall

It is past time that we end this farce of bail-in, which is nothing more than a scam to prop up banks’ gambling debts with their customers’ and investors’ savings, and instead impose real restrictions on financial gambling. And that means breaking up the banks along the Glass-Steagall division of commercial banks from investment banking and other financial services.

Glass-Steagall works! It protected the USA’s banks from systemic crises while it was in force from 1933 to 1999, and it’s what Australia needs to protect the people from the risks building up in our banking system. Whether or not the Hayne royal commission’s final report due 1 February recommends it, the CEC has legislation in Parliament ready to go, the Banking System Reform (Separation of Banks) Bill 2018, that will do the job.

What you can do

Phone, email or write to your Member of Parliament to demand they:

Break up the banks, by passing Banking System Reform (Separation of Banks) Bill 2018.

Audit the Big Four banks, using the Auditor-General, to assess the risk of a banking crash.

The Real Truth About Sleep and Exercise in the Cancer Fight

Studies show that there is a definite link between cancer and physical activity. Regular exercise reduces your personal risk of cancer but if you don’t get enough sleep, you could cancel out the positive effects of your workouts.

Is Overpersonalisation Killing the Variety and Interest of Your User Experience?

One user even noted that because the content was boring she continued to scroll looking for something that was interesting, “I don’t find anything interesting on Facebook tonight but what’s funny is that I will keep scrolling until I do; it’s addicting.” This behavior is related to the Vortex phenomenon, which refers to people feeling sucked into the online world almost against their will through sticky design techniques (like continuous content feeds). Users seek the emotional payoff they get from a good piece of content. In these cases, the phone turns into a mini slot machine: they keep pulling the lever coming across dozens of losers in hopes of finally getting a winner.